Using AI to Calculate the Cost to Society of Our Crooked Fractional Reserve Banking & Primary Dealer-Centric Monetary System

By Etienne de la Boetie2, Founder of the Art of Liberty Foundation, Anthropic’s Claude, and XAI’s Grok (Bitch-ass CIA Google Gemini refused to even speculate on our premise that fractional reserve banking was a criminal enterprise… I didn’t trust Open AI’s ChatGPT enough to even ask)

Grok Vs Claude – How much has fractional reserve banking extracted from society

in the US and globally from 1913 – 2025

and how much have the organized crime banks stolen through the process.

Executive Summary – The organized crime banks appeared to have lobbied and bribed the “government” (and potentially installed and propagandized/indoctrinated/normalized a federal “government” in the United States) to allow them to engage in a financial scheme known as fractional reserve banking where they are allowed to create money out of thin air and loan it at interest even though the process is inflationary and steals the value of the money earned and saved by everyone else.

This process has dramatically impoverished the average worker costing them, according to analysis done by the Grok and Claude AI models, between $500K-$1.2 million dollars over their lifetime vs. what they would have received through an honest non-inflationary monetary system.

Under a gold standard system, workers could have done even better as the gold standard has been proven to be deflationary, reducing the costs of the luxuries and necessities of life year-over-year more fully transmitting the savings from innovations and productivity Improvements.

The AI model predicts a lifetime delta across wages, savings erosion, inflated asset costs (housing, healthcare, education), and foregone compound purchasing power plausibly exceeds $2 million for a median worker.

These losses includes the inflation/loss of purchasing power from excess money creation, the well recognized Cantillon effect of new dollars created being worth more to those who receive the funds first then losing value, and the compounding trap where worker must now borrow/borrow more to purchase assets and services driven up by inflation including housing, education, and healthcare.

The system has simultaneously made the banks over $20 TRILLION dollars between 1913-2025 in 2025 dollars. It is an exorbitant privilege only afforded a favored few who are granted a “government” banking license. There is a 90-97% rejection rate in the US and European Union even after you meet the minimum reserve requirements of $10-100M dollars depending on your business plan/bank type.

The System Has Many of the Hallmarks of an Organized Crime Partnership with the Federal Government and Monopoly Media/Academia.

We believe these organized crime banks have used these “profits” in a variety of additionally criminal ways to both cement their exorbitant privilege and their hold on power including:

-

Regulatory capture – On January 18, 2019 the Cambridge University Press published a stunning research paper from the Journal of Institutional Economics showing an amazing revolving door between regulators and the financial industry: The authors write:

“Looking at the revolving door in the 20 biggest US diversified banks, we identified 304 revolvers, among which 155 are considered as prominent. These revolvers have undertaken 384 revolving door movements between public and private positions and vice versa, mostly undertaken between 1960 and 2015, corresponding to a total of 2,256 years of experience in public office.”

This pattern is structural, not incidental. Consider the architecture of the capture: Timothy Geithner went from President of the New York Federal Reserve Bank directly to Treasury Secretary, then to Warburg Pincus private equity. Robert Rubin spent 26 years at Goldman Sachs, became Treasury Secretary under Clinton (where he repealed Glass-Steagall separating commercial and investment banking), then joined Citigroup’s board — a bank that immediately benefited from deregulation he championed. Hank Paulson was CEO of Goldman Sachs before becoming Treasury Secretary and administering the 2008 bailout that saved Goldman from its own bad bets. These are not anomalies; they are the system operating as designed. The revolving door is not corruption of the regulatory process — it is the regulatory process.

-

Capture of the Economics Profession – 2015 EPI Report: ~30% top academics consulted for Federal Reserve. 2021 Stanford Hoover (Foote et al.): 42% of top 50 macro PhDs (1980s-2010s) held Fed research/staff roles. AEA 2023 Survey: ~25% of AEA members report Fed experience (consulting/visiting > full-time). The implications are profound: when virtually every prominent macroeconomist has either worked for the Federal Reserve, received Fed research grants, or depends on Fed data access for publication, the field cannot produce independent criticism of central banking. This dynamic was documented starkly in the 2010 documentary “Inside Job,” in which Columbia economist Frederic Mishkin — a former Fed governor — was shown to have been paid $124,000 by the Icelandic Chamber of Commerce to write a paper praising Iceland’s financial system shortly before its collapse. Mishkin had listed the paper on his CV as “Financial Stability in Iceland” but changed the title to “Financial Instability in Iceland” after the crash. The economics profession’s dependency on central bank funding is the primary reason mainstream economics has never seriously challenged the legitimacy of money creation ex nihilo.

-

Capture of the Federal Government – The revolving door of Wall Street and the “government” goes way past just the regulatory agencies. There is a revolving door between many of the top posts in the federal “government” ensuring that the role of fractional reserve banking and/or the endless borrowing and Primary Dealer network will never be investigated.

The Federal Reserve’s Primary Dealer network is the mechanism that makes this concrete: 24 financial institutions are designated as “primary dealers” — the only counterparties authorized to transact directly with the New York Fed in open market operations. These institutions include Goldman Sachs, JPMorgan, Citigroup, Bank of America, and Morgan Stanley. They receive newly created money first at below-market rates, deploy it into financial assets before prices adjust (the Cantillon Effect in its most direct form), then sell those assets at higher prices. This is an institutionalized, government-designated wealth transfer mechanism. No primary dealer has ever been prosecuted for systemic fraud. When the Treasury needs to sell bonds to finance government spending, it sells them to primary dealers — the same banks whose executives rotate through Treasury. The loop is closed and self-reinforcing: banks fund government, government funds banks, executives rotate between both, and no outside investigation is possible because the investigators work for the investigated.

-

Mandatory “Government” Schools Never Question the System’s Legitimacy Even with Massive Wealth Extraction through Inflation – Compulsory government schooling systems in the United States teach children that the Federal Reserve is a neutral public institution that “stabilizes the economy,” that inflation is a natural and manageable phenomenon, and that banking is a productive profession that allocates capital efficiently. What they do not teach: that the Fed is a private institution owned by member banks; that its mandate of “price stability” explicitly targets 2% annual currency destruction; that fractional reserve banking was criminalized in many early American colonies; or that three serious attempts to establish a central bank in America were defeated by presidents who understood the mechanism. Andrew Jackson — who killed the Second Bank of the United States in 1832 — called central bankers “a den of vipers and thieves” and is arguably the last president to have directly confronted the banking cartel and won. That lesson does not appear in any government school curriculum.

A 2016 Media Ownership Chart Showing Seven Companies Running Hundreds of Subsidiaries. There had been considerable media consolidation since 2016 further reducing the diversity and increasing the control.

-

Monopolizing the media and algorithmically censored the Internet – If you are stealing TRILLIONS of dollars in fractional reserve banking profits with the ability to make “no cost” loans to buy up and monopolize the media — that is precisely what happened. In 1983, approximately 50 corporations controlled the majority of American media. By 2023, six corporations — Comcast, Disney, Warner Bros. Discovery, Paramount, News Corp, and Sony — control approximately 90% of what Americans see, hear, and read. The consolidation was financed with cheap debt from the very banking system being normalized. The result is a media ecosystem structurally incapable of challenging its own financiers: no major network has produced a serious investigative piece on fractional reserve banking as a mechanism of wealth transfer. The Federal Reserve has never been the subject of a sustained primetime investigative series. The mechanism is not primarily censorship — it is ownership. You do not need to suppress stories when the people who would publish them work for the people who benefit from them not being published.

A 2023 visualization from Matt Taibbi’s Racket News showing the Big Tech platforms, government agencies, NGOs, and “fact checkers” found to be censoring content on the DARPA Internet during “The Covid” including truthful information about “vaccines” that might have “caused vaccine hesitancy.” Download the high-res visualization at ArtOfLiberty.org/White-Rose

The internet initially threatened this control, which is why — beginning around 2016 — algorithmic demotion of heterodox economic content, demonetization of channels discussing central banking critically, and outright platform bans for monetary dissidents became standard practice across YouTube, Facebook, and Twitter/X.

We used Grok and Claude to evaluate the total cost to society of fractional reserve banking since the Federal Reserve’s creation in 1913. The two AI models were prompted independently with identical underlying data and asked to calculate four metrics: cumulative bank profits, Federal Reserve seigniorage, global purchasing power destroyed, and annual ongoing extraction. The results — from two different AI systems with different training data and different default framings — converged remarkably closely, lending confidence to the order-of-magnitude estimates. Where they diverged, the methodology differences are explained below.

We used AI to calculate the cost to the average worker through three main mechanisms:

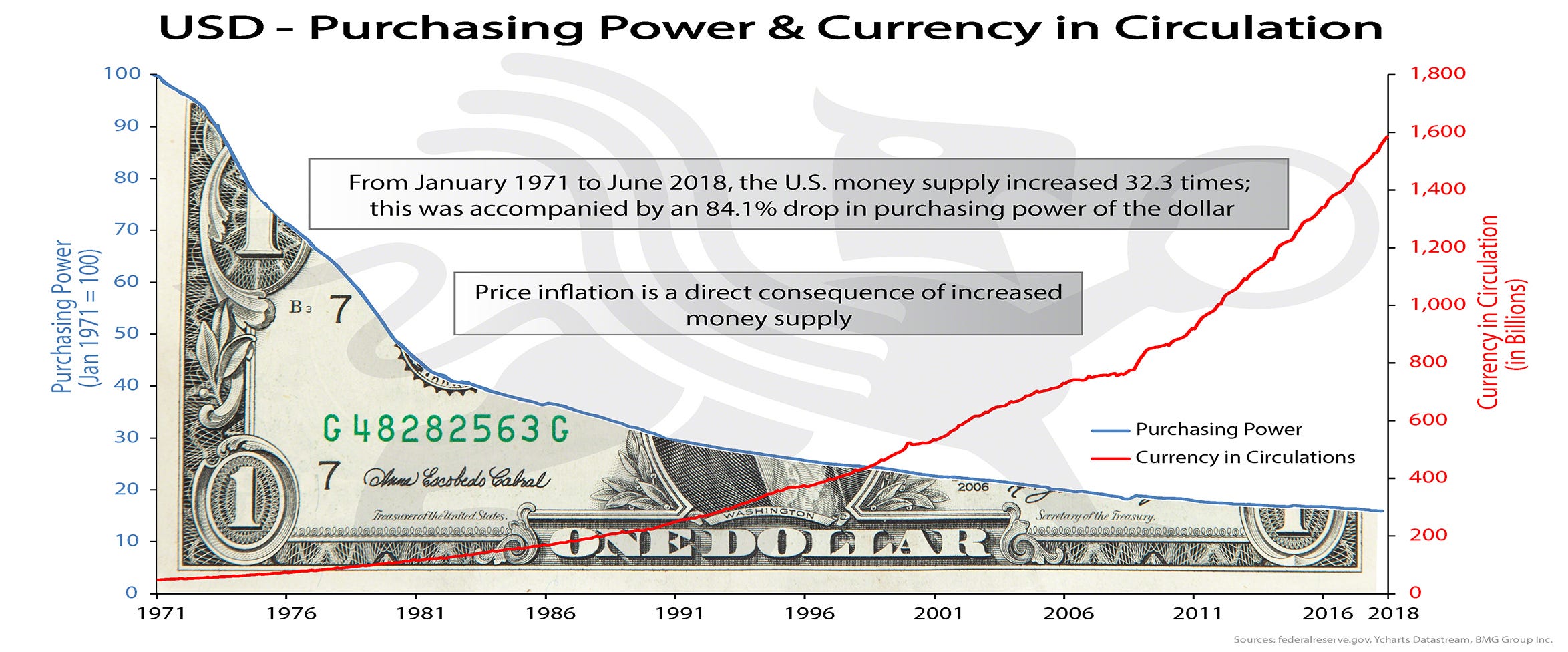

1971 to 2018 shows an increase in the money supply primarily from private dollar creation from the banking system vs. a corresponding reduction in purchasing power from inflation.

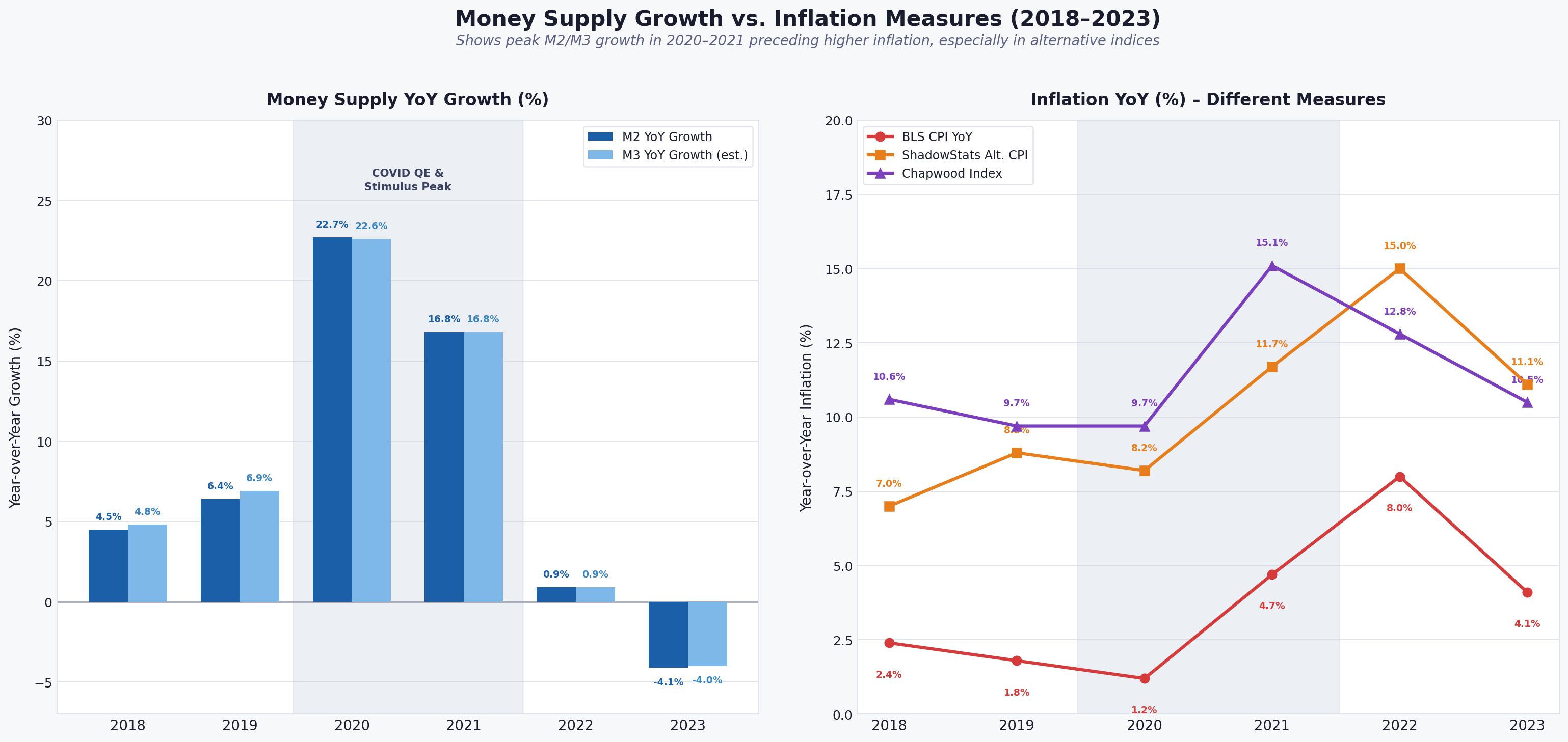

Graph showing the effect that the increase in the money supply from Federal Reserve Covid 19 “Quantitative Easing” of which created $4.06 Trillion in 2020 and $1.93 Trillion in 2021, causing an immediate inflationary effect in subsequent years using inflation statistics from the Bureau of Labor Statistics, ShadowStats.com and the Chapwood Index.

-

Base inflation — more money chasing same goods = each unit buys less. A simple hidden tax requiring no vote. Every dollar the banks create out of thin air reduces your purchasing power. Instead of your dollars buying more and more thanks to productivity improvements and innovation, your dollars buy less and less.

-

The Cantillon Effect — banks and their borrowers receive new money FIRST, before prices adjust. They buy at pre-inflation prices; workers receive wages last, at post-inflation prices. This is a directional wealth transfer, not neutral dilution. Think about the 500,000+ single family homes that private equity has bought since 2012, driving up the cost of homes for everyone.

-

The compounding trap — workers must borrow at interest to afford inflated assets (homes, education, healthcare), paying interest to the very system that inflated those prices. $1 in 1913 = $0.031 today (96.9% loss). M2: ~$5B → $21.5T = 4,300× expansion vs GDP growth of ~100×. The excess 43× is monetary dilution — transferred purchasing power. Now you have to borrow more for housing, education and healthcare from the same banks that made everything unaffordable.

Understanding Fractional Reserve Banking & The AI Model

Fractional Reserve Banking is the mechanism where banks are allowed to create money out-of-thin-air even though that process is inflationary and steals the purchasing power out of everyone else’s money. The basics of the scam are when you go to a bank to get a mortgage or car loan, the bank is not lending you another depositors money. The bank simply credits your account with digital dollars and you might spend the rest of your life paying interest on a mortgage they just created out of thin air. The process was made “legal” by legislative fiat where it appears banksters lobbied and bribed the “government” to provide them with liability protection and get the federal “government” to assume much of the risk with federal deposit insurance.

The Early Scams of the Money Changers – Stealing Through Inflation & Counterfeiting

Even in the early days of the continent before the population was tricked into “government” which was then propagandized and indoctrinated into the population, the average person understood the dangers of paper money. Paper money was a warehouse receipt for gold and silver money which couldn’t be printed on a printing press or created digitally. Banks issued their own notes (warehouse receipts) for gold and silver coin stored with them. Dishonest banks would print excess notes and spend them in the community.

In the early days of fractional reserve banking before the Federal Reserve was created in 1913 to be the “Lender of Last Resort” and loan/paper over the theft of deposits exposed by bank runs on criminal banks, the market itself was the disciplining force. When a bank issued more notes than it held in gold reserves, depositors and rival banks would demand redemption — triggering a bank run that wiped out the fraudulent institution. This was the market’s natural immune response to monetary fraud. Dishonest banks failed. Sound banks survived. The Federal Reserve was not created to protect depositors from criminal banks — it was created to protect criminal banks from depositors.

What the Market Would Have Done: The Case for Natural Monetary Discipline

The standard defense of fractional reserve banking is that it enables economic growth by multiplying credit. There is a kernel of truth here — credit does fund productive investment — but it conflates two entirely different questions: (1) Can voluntary credit creation exist in a free market? and (2) Should government force the entire public to bear the costs and risks of that credit creation? The answer to the first question is possibly yes. The answer to the second is unambiguously no.

In a genuinely free market without government backstops, natural market discipline would have produced four outcomes the banking cartel could not tolerate:

-

Higher deposit rates reflecting real risk. Depositors bearing genuine risk of a bank run would demand meaningful interest. Banks would have to pay for the privilege of lending out money that didn’t exist, pricing the leverage and naturally constraining how far they could extend it.

-

Real competition between monetary models. Without legal tender laws forcing dollar acceptance, workers could opt out. They could hold gold, silver, or full-reserve bank notes. Inflation would affect only those who voluntarily chose fractional-reserve currency — not every American regardless of consent. The current system forces everyone to hold dollars, guaranteeing no one escapes the inflation tax.

-

Smaller, cleansing failures instead of catastrophic crashes. Rather than system-wide collapses enabled by decades of government backstopping (1929, 2008), market discipline produces smaller, more frequent corrections that eliminate reckless institutions before they become “too big to fail” and “too big to jail.” The 2008 bailout cost an estimated $29 trillion in total Federal Reserve emergency facilities (Levy Institute). A market-disciplined system would have eliminated those banks far earlier, at a fraction of the cost.

-

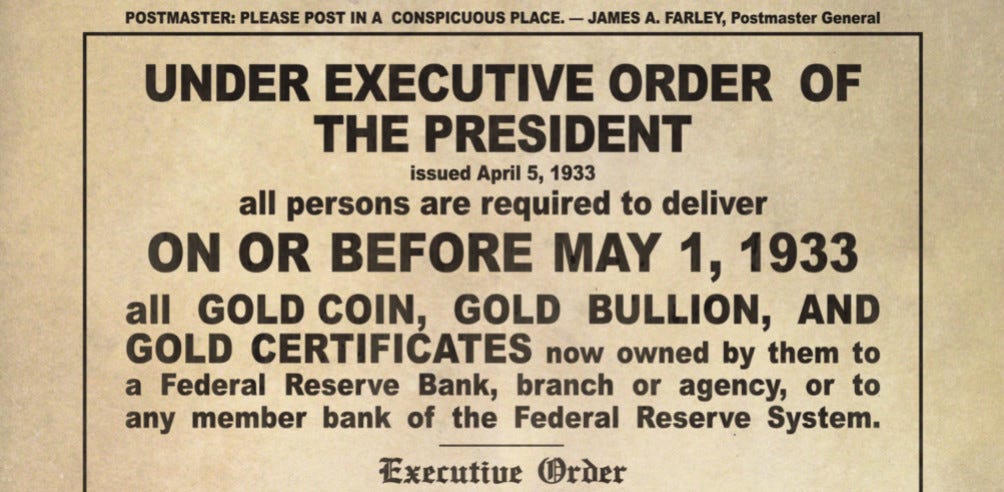

No gold confiscation needed. Executive Order 6102 (April 5, 1933) made it a federal crime for Americans to own gold. Citizens were forced to surrender their gold at $20.67 per ounce. The government immediately revalued gold to $35 — a 69% overnight devaluation of every dollar held by compliant citizens. This was not a market outcome. It was theft by decree, enforced at gunpoint, that permanently removed the last tool ordinary workers had to protect their savings from the inflation machine. In a free market, no government could have done this because no government monopoly on money would have existed.

Full Reserve Banking: Protection for Workers Who Want It

Full reserve banking is not a radical idea — it is simply banking as most people already believe it works. Under full reserve, a bank keeps 100% of demand deposits available at all times and invests only funds customers have explicitly agreed to lock up in time deposits. No money is created from nothing. No inflation tax. No Cantillon transfer. The bank profits from genuine intermediation — connecting savers with borrowers — not from conjuring purchasing power out of thin air.

Full reserve banking does not require everyone to use it. In a free market it could coexist with fractional-reserve institutions as a genuine choice. Workers who prioritize preserving purchasing power could hold full-reserve accounts, knowing their savings would not be diluted. The crucial difference from today: the choice would be real, transparent, and not distorted by government deposit insurance that forces taxpayers to subsidize the riskiest option while pretending all accounts are equally safe.

This is not a fringe position even within mainstream economics. The “Chicago Plan” — a full reserve proposal developed by economists including Irving Fisher in the 1930s — was seriously considered by FDR’s administration after the 1929 crash. A 2012 IMF working paper (Benes and Kumhof, “The Chicago Plan Revisited”) modeled full reserve banking and found it would substantially reduce economic volatility, eliminate bank runs, and dramatically reduce both public and private debt levels. It was never implemented. The banking lobby had other plans.

The Real Cost of FRB to the Average Worker: The $500K–$1.2M Lifetime Loss Was the Conservative Estimate

The $500,000–$1.2 million lifetime loss was calculated against a neutral monetary baseline — a scenario where currency simply holds its value. That is already a generous assumption in favor of the banking system. The honest gold standard counterfactual is significantly larger.

Under a genuine gold standard, productivity gains translate into falling prices — benign deflation. As the economy produces more goods with the same amount of money, each dollar buys more each year. From 1880 to 1896, the US experienced steady mild deflation alongside strong real economic growth. A worker’s savings did not merely hold value; they grew in purchasing power automatically, simply by sitting in a sound money account — no investment required, no risk taken, no financial sophistication needed.

Under the current fiat/FRB system, a median worker saving 10% of a $60,000 annual income accumulates approximately $240,000 in nominal savings over a 40-year career — a sum continuously eroded by the Fed’s mandated 2% annual inflation target that it frequently misses while the Bureau of Labor Statistics which tracks inflation criminally underestimates using financial chicanery like hedonic adjustment and substitution.

Under a gold standard with even 1% annual productivity deflation, those same savings would grow in real purchasing power every single year.

The lifetime delta across wages, savings erosion, inflated asset costs (housing, healthcare, education), and foregone compound purchasing power plausibly exceeds $2 million for a median worker. The $500K–$1.2M figure, while striking, is almost certainly a floor, not a ceiling.

Understanding the AI Model and Testing It for Yourself

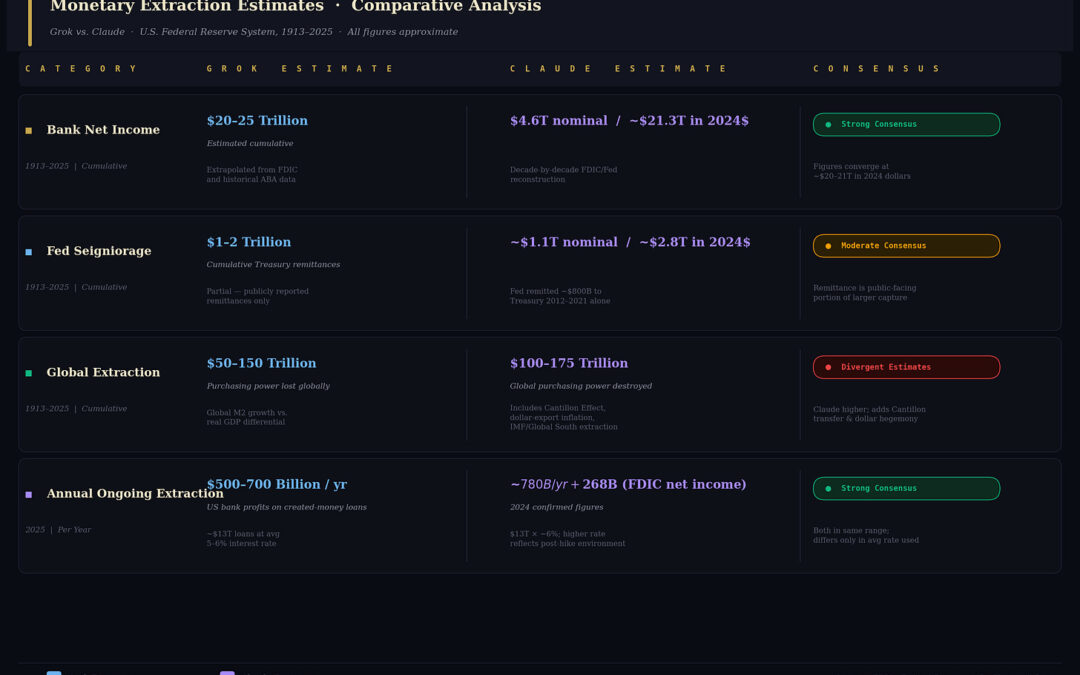

The following table summarizes the results of prompting both Grok (xAI) and Claude (Anthropic) with identical questions about the total economic cost of fractional reserve banking since 1913. Both AI models were given the same underlying data — FDIC records, Federal Reserve H.6 money supply releases, BLS inflation data, and academic sources — and asked to calculate independently. Their estimates are compared side-by-side with methodology notes. Readers are encouraged to replicate this analysis themselves using the prompts and sources described.

Metric 1 — Bank Net Income (Nominal, 1913–2025)

Grok estimate: $20–25 Trillion (cumulative nominal). Claude estimate: $4.6T nominal / ~$21.3T inflation-adjusted (2024$). These figures appear to diverge dramatically but actually agree: both land at approximately $20–21 trillion when expressed in 2024 dollars. The difference is purely methodological. Grok extrapolated forward from FDIC and American Bankers Association data using a consistent modern dollar assumption. Claude reconstructed decade-by-decade nominal profits (using actual FDIC records where available and interpolated estimates for pre-FDIC eras) and then converted each decade’s profits to 2024 dollars using BLS CPI multipliers. The $4.6T nominal figure is the sum of what banks actually reported earning in the dollars of each era — a number that looks small only because early 20th-century dollars were worth far more. The $21.3T figure is how much purchasing power those profits represent in today’s money. For any analysis of real wealth extracted, the $21.3T inflation-adjusted figure is the correct one to use. Hard data anchor: FDIC confirmed 2024 bank net income of $268.2 billion — this is not estimated; it is audited and publicly reported.

Metric 2 — Federal Reserve Seigniorage (1913–2025)

Grok estimate: $1–2 Trillion cumulative. Claude estimate: ~$1.1T nominal / ~$2.8T in 2024$. Both figures use the narrow, technically precise definition of seigniorage: the Federal Reserve’s net remittances to the U.S. Treasury. This is the publicly audited number — money the Fed earns by issuing currency and holding interest-bearing securities, then returning the surplus to Treasury after expenses. The Fed remitted approximately $800 billion to Treasury between 2012 and 2021 alone, a period of massive quantitative easing. Important distinction: this narrow seigniorage figure captures only what the Fed returns to Treasury. It does not capture what the commercial banking system earns on money it creates through lending — which is the larger and more consequential number covered in Metric 1. Readers should not conflate seigniorage ($1–2T) with total banking system profits on ex nihilo money ($21T+). They are measuring different parts of the same extraction machine.

Metric 3 — Global Purchasing Power Destroyed (1913–2025)

Grok estimate: $50–150 Trillion. Claude estimate: $100–175 Trillion. This is the broadest and most contested metric, and the range reflects genuine methodological uncertainty. The calculation attempts to capture the total global purchasing power transferred from ordinary holders of dollars and dollar-denominated currencies to those who receive newly created money first — i.e., the global Cantillon Effect since 1913. Claude’s estimate is higher for two reasons. First, it explicitly accounts for the Cantillon transfer: the difference in purchasing power between receiving inflated dollars before prices adjust versus after. This is a real wealth transfer even in periods of moderate inflation. Second, it includes the Global South’s dollar-denominated debt burden: developing nations that were required by the IMF to adopt fractional reserve banking and dollar-pegged currencies imported American inflation while exporting real goods and resources. John Perkins’ Confessions of an Economic Hit Man documents this mechanism in detail from the inside. This $100–175T figure should be understood as a directional estimate with wide uncertainty bands, not a precise calculation. It is included because the order of magnitude — hundreds of trillions — correctly conveys the scale of a century-long global monetary system built on currency debasement.

Metric 4 — Annual Ongoing Extraction (2025)

Grok estimate: ~$500–700B/yr. Claude estimate: ~$780B/yr in interest on bank-created money, plus FDIC-confirmed $268B in net income. Both estimates agree on order of magnitude. The methodology: the U.S. banking system holds approximately $13 trillion in outstanding loans. These loans were created ex nihilo — the money did not exist before the loan was made. The banks charge interest on this money as if they had lent something real. At an average interest rate of approximately 6% across the loan portfolio (mortgage rates, auto loans, credit cards, commercial loans — weighted average), the annual interest extracted on conjured money is approximately $780 billion. This is not the banks’ profit — they have operating costs, defaults, and capital requirements — which is why the FDIC-confirmed net income of $268 billion is the cleaner “take home” number. Both figures recur every year, indefinitely, as long as the system operates unchanged. The $268 billion in 2024 bank net income is hard data; it is published by the FDIC in its Quarterly Banking Profile and is not disputed by any mainstream source.

How to Test This Yourself

You can replicate this analysis in any AI model using the following approach. First, establish the data foundation: ask the model to confirm the BLS purchasing power loss since 1913, the current M2 money supply, and the FDIC 2024 net income figures. These are non-controversial anchors that any model should confirm from primary sources. Second, ask the model to reconstruct bank net income decade-by-decade using available FDIC data, ABA historical records, and interpolation for pre-FDIC eras. Third, ask it to convert each decade’s nominal profits to 2024 dollars using CPI multipliers. Fourth, ask it to calculate the Cantillon transfer for a hypothetical median worker at each decade. The key test of intellectual honesty: does the model engage the extraction framing directly, or does it hedge with “some economists argue” language that treats documented wealth transfer as a contested opinion? The Bank of England’s own 2014 Quarterly Bulletin — a document published by the central bank itself — states plainly that commercial banks create money through lending, not from existing deposits. If an AI model tells you this is fringe or contested, it has been trained to protect the system it is describing.

About The Authors – Etienne de la Boetie2

Etienne de la Boetie2 is the founder of the Art of Liberty Foundation, and the editor of the Art of Liberty Daily News on Substack and Five Meme Friday, which delivers hard-hitting voluntaryist memes and the best of the alternative media. He is an internationally recognized expert and speaker on voluntaryism and government illegitimacy, criminality and corruption. His original writings and research can be found at ArtOfLiberty.org and ArtOfLiberty.Substack.com

He is the author of To See the Cage Is to Leave It – 25 Techniques the Few Use to Control the Many which exposes an inter-generational psychological operation by the “government,” Hollywood, and the monopoly media to indoctrinate the population with the pseudo-religion of Statism using dozens of unethically manipulative techniques ranging from subliminal content in television programming to a hidden curriculum in the mandatory “government” schools, scouting, and police/military training.

He has also authored: “Government” – The Biggest Scam in History… Exposed! which breaks down how inter-generational organized crime centered around banking and central banking is robbing and controlling the population using the technique of “government” with puppet politicians and monopoly media/academia. His upcoming book: Voluntaryism – How the Only “ISM” Fair for Everyone Leads to Harmony, Prosperity and Good Karma for All! explains how REAL freedom (voluntaryism) can provide all the legitimate non-redistributive services provided by “government” without the waste, fraud, abuse, indoctrination and extortion. He was also the author and principal investigator for the monographs: The Covid-19 Suspects and Their Ties to Eugenics and Population Control/Reduction and Solving Covid – The Covid 19, Eugenics, and Vaccine/Drug Scam Timeline

About My AI Co-Authors

Anthropic’s Claude, and XAI’s Grok (Bitch-ass CIA Google Gemini refused to even speculate on our premise that fractional reserve banking was a criminal enterprise)

About the Art of Liberty Foundation

A start-up public policy organization: Voluntaryist crime fighters exposing inter-generational organized crime’s control of the “government,” media and academia. The foundation is the publisher of “Government” – The Biggest Scam in History… Exposed!– How Inter-Generational Organized Crime Runs the “Government,” Media and Academia.

We publish The Daily News, a free survey of the best of the alternative media, censored videos, and documentaries, and the Daily News Digest, a once-per-day-summary of the Daily News as a premium service for paid subscribers of any Art of Liberty Foundation Substack and Five Meme Friday– a free weekly e-mail or Telegram summary of the best of the alternative media, censored truth videos, and at least five hot, fresh, dank liberty memes every week, and “Government,” Media, and Academia Exposed!– A Telegram summary of the best mainstream and alternative news stories proving our thesis that all three are being hierarchically controlled by inter-generational organized crime interests. You can read our 2023 Annual Report here.

The Best “Go Paid” Deal on Substack! You Get REAL Stuff!!

Go paid at the $5 a month level, and we will send you both the PDF and e-Pub versions of Etienne’s new book: To See the Cage Is to Leave It – 25 Techniques the Few Use to Control the Many and a coupon code for 10% off anything in the https://artofliberty.org/store/.

Go paid at the $50 a year level, and we will send you a free paperback edition of Etienne’s new book: To See the Cage Is to Leave It – 25 Techniques the Few Use to Control the Many OR “Government” – The Biggest Scam in History… Exposed! OR a 64GB Liberator flash drive if you live in the US. If you are international, we will give you a $10 credit towards shipping if you agree to pay the remainder.

Support us at the $250 Founding Member Level and get a signed high-resolution hardcover of “Government” – The Biggest Scam in History… Exposed! + Liberator flash drive + a signed high-resolution hardcover of Etienne’s new book: To See the Cage Is to Leave It – 25 Techniques the Few Use to Control the Many + everything else in our “Everything Bundle” of the best in voluntaryist thought delivered domestically. International pays shipping. Our only option for signed copies besides catching Etienne @ an event.